1. Review of domestic polyester filament market conditions from January to June 2021

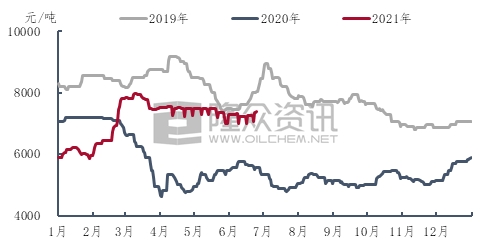

In the first half of 2021, domestic polyester filament prices showed a trend of fluctuation after rising. From the beginning of the year to mid-March, with the support of the cost side, factory production and sales increased, and filament prices continued to rise. Taking POY 150D/48F as an example, it rose from 5,900 yuan/ton at the beginning of the year to 7,975 yuan/ton in mid-March. More than 2,000 yuan/ton.

Figure 1 Polyester filament POY 150D/48F price trend from 2019 to 2021

Source: Longzhong Information

Table 1 Domestic polyester filament price statistics unit: yuan/ton

Source: Longzhong Information

Then polyester filament began to show a volatile trend. In more than 2 months, periodic promotions gradually became the norm. At first, it was once every half a month, and gradually evolved into once a week. However, due to poor demand performance, market focus and promotional results have gradually declined. Compared with the level in April, the market focus of POY 150D/48F in June has dropped by more than 200 yuan/ton.

2. Analysis of domestic polyester filament supply and demand data from January to June 2021

1. Supply analysis from January to June 2021

Table 2 Domestic polyester filament production capacity and output changes Unit: 10,000 tons/year

Source: Longzhong Information

From the perspective of production capacity, Due to the elimination of some long-stop direct spinning polyester filament devices at the beginning of 2021, the current domestic production capacity is slightly less than the end of 2020, but the effective production capacity data has increased significantly. From the perspective of output, under the low base effect, output increased significantly in the first half of the year. From January to June, domestic polyester filament output was 14.6253 million tons, an increase of 14.52% compared with the same period in 2020.

Table 3 Overview of domestic polyester filament production capacity changes in 2021 Unit: 10,000 tons/year

Source: Longzhong Information

Figure 2 Domestic polyester filament output and operating rate changes in 2021

Source: Longzhong Information

From the perspective of output and start-up conditions, from the beginning of the year to mid-February, the output and load of polyester filament gradually declined. With the arrival of the Spring Festival, it fell to the lowest level of the year in mid-February. With the improvement of market demand, the volume and price of polyester filament increased. With the successive commissioning of new equipment, the output and load of polyester filament also began to recover rapidly, and in It rose to the highest level of the year in April. However, terminal demand did not show a substantial improvement in the second quarter, and when production and sales continued to be poor, polyester filament FDY profits declined rapidly. Affected by this, mainstream FDY factories mostly reduced production and overhauled, and domestic polyester filament output and load declined. It must be declining. After entering June, some early production reduction and maintenance equipment increased the load. The output and load of polyester filament increased in a narrow range, and then the performance was relatively stable.

Table 4 Changes in polyester filament import and export data in the first five months of 2021 Unit: 10,000 tons

Source: General Administration of Customs

Domestic polyester filament exports have shown rapid growth this year. According to customs data, in 2021 In the first five months, domestic polyester filament exports were 1.3823 million tons, a sharp increase of 42.94% compared with the same period last year. Compared with the same period in 2019, there is also a compound growth rate of more than 10%. From the perspective of imports, my country, as the world’s major polyester filament producing country, has the most complete upstream and downstream supporting facilities, and with the continuous increase in domestic polyester filament production capacity, the overall import volume is at a low level. Judging from the import volume from January to May, it was only 49,100 tons, which was less than a fraction of the domestic polyester filament export volume during the same period.

2. Demand analysis from January to June 2021

Add The elastic belongs to the post-spinning part of the upstream polyester filament and is the direct downstream user of polyester filament POY. Last year, the overall profit of DTY was at a relatively high level. In addition, downstream users are optimistic about the market outlook. This year, the growth rate of texturing machines has expanded. As of July this year, it is expected that the number of new texturing machines will include about 1,500 domestic and foreign brands. In the first half of the year, the terminal weaving start-up was relatively stable. Compared with the start-up in March-April 2019, the difference between the higher start-up and the start-up was about 10%. The terminal domestic and foreign trade orders gradually entered the recovery stage.

Figure 3 Comprehensive weaving start-up rate in Jiangsu and Zhejiang from 2019 to 2021

Source: Longzhong Information

After the Spring Festival, the price of polyester filament continued to reach new heights. Downstream users did not stock up in time. Resistance to high prices gradually increased, and the inventory of polyester filament companies increased accordingly. April toPolyester filament prices have fluctuated and dropped, cost pressure has eased, domestic and foreign trade customers have placed orders more frequently, and texturing and weaving operations have gradually entered a stable period. In particular, weaving operations in May were higher than the same period in previous years. It is understood that since May, some downstream weaving companies have started purchasing and stocking up for autumn and winter orders in advance. Due to good market demand expectations in the second half of the year, most weaving companies have chosen to stock up on conventional gray fabrics in advance, which has led to the advance timing of raw material procurement. Taken together, the global economic recovery is still in the repair stage. The current overdraft of the autumn and winter market in advance does not fully represent the real release of demand. According to historical data in previous years, weaving starts gradually increased in August and gradually increased in mid-to-late September. However, this year’s weaving orders have shown a pattern of small batches and multiple orders, and the weaving market in the second half of the year may last for up to two months.

3. Analysis of inventory data of domestic polyester filament companies from January to June 2021

In 2021, the polyester filament inventory has two highs and one low, with the low point appearing in January and February. Since October last year, terminal footwear, clothing and home textile orders have been placed in large quantities, weaving starts have reached historical highs, and the demand for raw material stocking has once been The increase coupled with the fact that the price of polyester filament was at a historical low last year, the frequency of shipments from upstream polyester factories has accelerated and inventories have been declining. However, after the Spring Festival holiday, the price of polyester filament in March increased to 500-800 yuan/ton compared with the pre-holiday position. The frequency of domestic and foreign trade orders slowed down. The polyester filament factory inventory climbed to 24.1 days. Although it is at a high level, it is still available. within the control range.

Table 5 Average annual inventory comparison of polyester filament in the first half of 2019-2021 Unit: day

Source: Longzhong Information

In May, terminal demand weakened for a time, with skyrocketing sea freight, rising exchange rates, and traditional Under the multiple influences of the off-season of the textile market, market circulation is hindered. The raw materials purchased from the downstream in the early stage have not been consumed. The procurement is mostly maintained as rigid demand. It is difficult to turn around under financial pressure. The polyester filament in the factory has reached a high point. Subsequently, temperatures will gradually increase and most areas will initiate power rationing policies. At that time, the start-up of some downstream weaving enterprises may further decline, and polyester filament factory inventories may increase.

IV. Cost and profit analysis of the domestic polyester filament industry from January to June 2021

Figure 4 Price and cost trend chart of mainstream polyester filament models

Source: Longzhong Information

Up The profit of polyester filament in the first half of the year has improved significantly compared with last year. Judging from the average profit in the first half of the year, POY150/48 is at 545 yuan/ton, FDY150/96 is at 297 yuan/ton, and DTY150/48 is at 275 yuan/ton. Judging from the average price in the half year, The model with the best profit in the first half of the year was POY. The overall performance of FDY and DTY was weak. On the one hand, the raw material end was favorable for polyester filament in the first half of the year. On the other hand, the demand-side texturing plant had a large new production capacity, which supported POY profits. . Therefore, the overall performance of the profit side is acceptable, but since June, the performance of the polyester raw material side has been strong, and the demand side has entered the traditional off-season, with demand constraints, and the profit of polyester filament has been rapidly squeezed to 50-200 yuan/ton.

5. Domestic polyester filament trend forecast from July to December 2021

According to Longzhong data, polyester filament yarn production capacity is expected to increase by 3.55 million tons in the second half of the year. The new production capacity is mainly concentrated in Jiangsu and Zhejiang. In addition, there are polyester filament yarn projects in Korla, Xinjiang and Weifang, Shandong. In the first half of the year, new production capacity will be added The production capacity is 800,000 tons. In August last year, a 600,000-ton unit of Hengke was put into operation, and yarn production continued until April this year. Overall, the new polyester filament production capacity in 2021 is expected to be 4.95 million tons, a year-on-year increase of more than 13%, and the terminal Consumption is expected to grow at 7%-8% throughout the year, which is lower than expected growth in production capacity. Therefore, the contradiction between supply and demand for polyester filament remains prominent in the second half of the year.

Table 6 Polyester filament production plan unit in the second half of 2021: 10,000 tons/year

Source: Longzhong Information

Looking at previous years, demand for polyester filament picked up during the “Golden Nine and Silver Ten” periods. Last year, despite the epidemic, the In late September and October, polyester filament yarns experienced a big rebound. Terminal demand exploded, and downstream users purchased in large quantities, driving up the price of polyester filament yarns. However, what is different from last year is that this year, downstream texturing and weaving companies have sufficient raw material stocks. As mentioned above, downstream users have started purchasing autumn and winter orders in advance since May, and demand has been overdrawn in advance. However, the overseas epidemic has not followed the vaccine. The epidemic has been effectively controlled through vaccination. At present, the overseas epidemic seems to have a counterattack trend. Polyester filament terminal fields are mostly used in textiles and clothing, with a large proportion of exports. Therefore, the overseas epidemic affects the export of textile and clothing. In addition, trade disputes, increased shipping costs, container Many problems such as tight supply have hindered the export of textiles and clothing. At present, the overall export situation of textiles is good, and the export volume of clothing continues to decline. Taken together, the activities of major e-commerce platforms in September and October promoted demand to a certain extent. However, the peak season may not be able to continue last year’s explosive growth in demand. In the third quarter, polyester filament inventory may decline slightly. If not Supported by other emergencies, inventories will gradually increase in the fourth quarter.

Under the influence of the epidemic, the price of polyester filament bottomed out again and again last year, falling to historical lows. At the end of the year, the price continued to recover due to the boost of costs. However, there is no obvious trend of recovery in terminal demand. Since the second quarter, polyester filament yarns have continued to boost volume with price, and the focus of transactions has continued to decline, reaching a relatively low point now. At the end of June, the destocking effect of enterprises was obvious. It is expected that in the second half of the year, polyester filament yarns will be in a stalemate at first, then rise first and then fall. Prices The high end appears in October and the low end appears at the end of December.

A slight downward trend, if not supported by other emergencies, inventories will gradually increase in the fourth quarter.

Under the influence of the epidemic, the price of polyester filament bottomed out again and again last year, falling to historical lows. At the end of the year, the price continued to recover due to the boost of costs. However, there is no obvious trend of recovery in terminal demand. Since the second quarter, polyester filament yarns have continued to boost volume with price, and the focus of transactions has continued to decline, reaching a relatively low point now. At the end of June, the destocking effect of enterprises was obvious. It is expected that in the second half of the year, polyester filament yarns will be in a stalemate at first, then rise first and then fall. Prices The high end appears in October and the low end appears at the end of December. </p